Roofing Materials Matter: Assessing Performance and Durability

The intersection of better data, scientific innovation, and roofing trends is leading to the development of new roofing solutions. The building materials industry is constantly evolving, and the ramping down of 3-tab asphalt shingle production in the U.S. market has notably affected property insurance carriers’ underwriting and claims processes. A mix of economic factors and consumer preferences has led most manufacturers to wind down production of 3-tab shingles. As a result, insurance carriers are adapting their underwriting and claims processes in response to the shift away from traditional 3-tab asphalt shingles. The move towards more durable roofing options influences overall claims costs, repair rates, and reconstruction expenses. This transition affects insurers’ approach to managing and processing claims more efficiently, as they navigate the implications of changing material performance on their policies.

The challenges faced by the insurance industry are not impossible to overcome. In fact, they are promoting innovation within the industry, creating tools, processes, and products that enhance operational efficiency and customer satisfaction.

Understanding Insurance Risk in Roofing

Insurance carriers consider various factors when evaluating the risks associated with different types of roofing materials. These factors are critical in making coverage and premium decisions.

Key Considerations for Evaluating Roof Material Risks by Insurance Carriers

Below are the key considerations associated with roof materials:

- Material Type: Different roofing materials offer varying levels of durability and resistance to common hazards such as wind, hail, and fire. Insurance providers assess the type of material used in roofing to gauge its ability to withstand potential damage.

- Age and Condition: The age and condition of a roof are pivotal factors in its susceptibility to damage. Older roofs, especially those nearing the end of their expected lifespan, may be considered at higher risk due to their heightened vulnerability to leaks, deterioration, and structural issues. This underscores the importance of regular maintenance and timely replacement.

- Installation Quality: The quality of installation plays a critical role in a roof’s performance and longevity. Insurance carriers may inquire about the roofing contractor’s credentials from the manufacturer’s installation programs and their reputation to ensure that industry best practices were followed during installation.

- Roof Slope and Design: The slope and design of a roof can influence its resilience to weather-related hazards. Steeper slopes and certain architectural features may reduce the likelihood of water pooling, snow accumulation, and wind uplift, lowering the risk of damage.

- Local Climate and Geographic Factors: Regional weather patterns, climate conditions, and geographic location can significantly influence a property’s risk profile. Areas prone to severe weather events such as hurricanes, tornadoes, or wildfires may face higher insurance premiums or specific requirements for roofing materials. This highlights the necessity of adapting roofing materials to the local environment to mitigate potential risks.

- Building Codes and Regulations: Compliance with local building codes and regulations is essential for ensuring a roof’s structural integrity and safety. Insurance carriers may verify that the roofing materials and installation methods meet or exceed mandated standards to mitigate risk.

- Availability: With over 75 million insured homeowners, about 5% file a claim annually, with wind and hail damage making up over 40% of these claims. Given the large volume of roofing materials purchased by insurance carriers, the ongoing limited supply of 3-tab asphalt shingles highlights a critical issue: material availability. This shift will affect how carriers manage underwriting, repair programs, and claims processing, emphasizing the need for adaptable solutions in the face of evolving material landscapes.

Importance of Performance and Durability in Mitigating Insurance Risk

Performance and durability are paramount considerations for insurance carriers when assessing risk related to roofing materials. Investing in high-quality, resilient roofing materials can yield significant benefits in risk mitigation and cost savings over the long term.

By prioritizing performance and durability in roofing choices, homeowners can reduce the likelihood of damage, minimize insurance claims, and enhance the overall resilience of their properties against unforeseen events.

Performance Assessment of Roofing Materials

Different roofing materials can vary broadly in their performance and durability. Depending on the geography of where the building is located, different materials may be better capable of withstanding that area’s unique weather conditions.

Roofing Material Dilemma: Strategies for Insurance Carriers

Roofing materials play a crucial role in determining the level of protection of a homeowner’s property against natural disasters, pests, and fire. Insurance companies consider the type of material selected while underwriting and covering homeowners’ policies since it can significantly affect the roof’s lifespan.

Repairing a roof rather than replacing it can be efficient, especially for localized damage. While asphalt shingles are prevalent, it’s important to note that many roofs use different materials. The challenge arises with 3-tab shingles, which are increasingly hard to match due to declining availability. itel’s analysis of thousands of shingles annually reveals that finding like-kind replacements for 3-tab shingles has become increasingly difficult, with the shortage growing by 34% over the past four years. This trend underscores the need for flexibility in repair strategies to accommodate various roofing materials.

If you’re interested in learning more about this trend and how it impacts property claims, we invite you to download itel’s white paper “Roofing Revolution: The Discontinuation 3-Tab Asphalt Roofing Shingles and the Impact on Property Claims“. This comprehensive white paper is a must-read for insurance carriers, providing valuable insights and recommendations to make informed decisions in the ever-evolving roofing industry.

How Roofing Choices Shape Insurance Claims

The roofing industry is constantly changing, which poses a challenge for insurance companies to keep up with the latest materials. Since the type of roofing materials used can significantly impact the frequency and severity of insurance claims related to property damage, insurance carriers must stay informed on the latest developments in the field to provide the best coverage to their clients. Consider the following data:

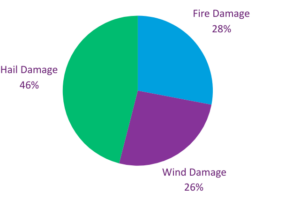

Cause of Damage in Asphalt Shingle Claims, 2023

itel data; based on approximately 1 million Asphalt Shingle Pricing tests

- Hail Damage: Properties with asphalt shingle roofs may experience more frequent hail damage claims than those with metal or tile roofs. The impact resistance of roofing materials determines the extent of damage and the need for repairs or replacements.

- Wind Resistance: During severe windstorms, roofs made of less durable materials may suffer from shingle uplift, tearing, or detachment, leading to water intrusion and interior damage. Metal and tile roofs offer superior wind resistance and are less prone to wind-related issues.

- Fire Protection and Other Claim Types: Properties in areas prone to wildfires, storms, and other natural catastrophes, including water damage, can greatly benefit from using fire-resistant and water-resistant materials. Such materials can help prevent ignition and spreading of flames in wildfires and minimize water damage caused by heavy rains and floods. Investing in fire-rated and water-resistant materials can result in lower premiums, improved property protection, and peace of mind.

Understanding the correlation between roofing material performance and insurance claims can help homeowners and insurers make informed decisions about risk management and coverage options. Stakeholders can mitigate risk, enhance property value, and promote long-term sustainability by prioritizing quality, durability, and resilience in roofing choices.

Industry Trends and Innovations

Jacob Piazza, Director of Roofing Services at itel, highlights a major shift in the roofing industry toward alternative roofing solutions. “Alternative roofing materials, such as metal roofing, are gaining significant market share year after year, reflecting a broader trend toward diversification in the roofing industry. “

Finally, Jacob notes that challenges are often greeted with opportunity, “technology and innovation are set to streamline processes and improve efficiency across the roofing supply chain. From eco-friendly and sustainable materials to digital tools for project management, technology is absolutely revolutionizing the roofing industry, impacting the entire insurance ecosystem.” Click to read our exclusive with Jacob about his thoughts on the discontinuation of 3-tab asphalt roofing shingles.

Sealing the Deal: Strengthening Roof Claims with itel Solutions

The roofing industry is experiencing rapid transformation due to the advancements in materials, technology, and collaboration among partners across the ecosystem. Embracing transparency, innovation, and strategic partnerships is crucial to ensure the long-term sustainability of properties and insurance operations. By working together to address challenges and seize opportunities, we can build a more resilient and prosperous future for homeowners, insurers, and the roofing industry.